Creating freedom in your life often starts with establishing consistent habits. This truth applies as much to achieving financial freedom as it does to enhancing your personal well-being through exercise or a balanced diet. Financial freedom isn’t a distant dream; it’s a tangible reality that can be built on the

As you reach your forties, you may begin thinking more about saving for retirement and whether you’re on the right track. It’s recommended that you have three times your annual salary saved by the time you reach 40. However, the average American between the ages of 40 and 49 had

The TriCapital Wealth Management team is excited to announce the firm’s 25th Anniversary! Founded on a simple premise, and with a commitment to excellence, they have been gratified to serve clients in Charlotte and the surrounding area since 1999. “We chose the name TriCapital 25 years ago because we operate

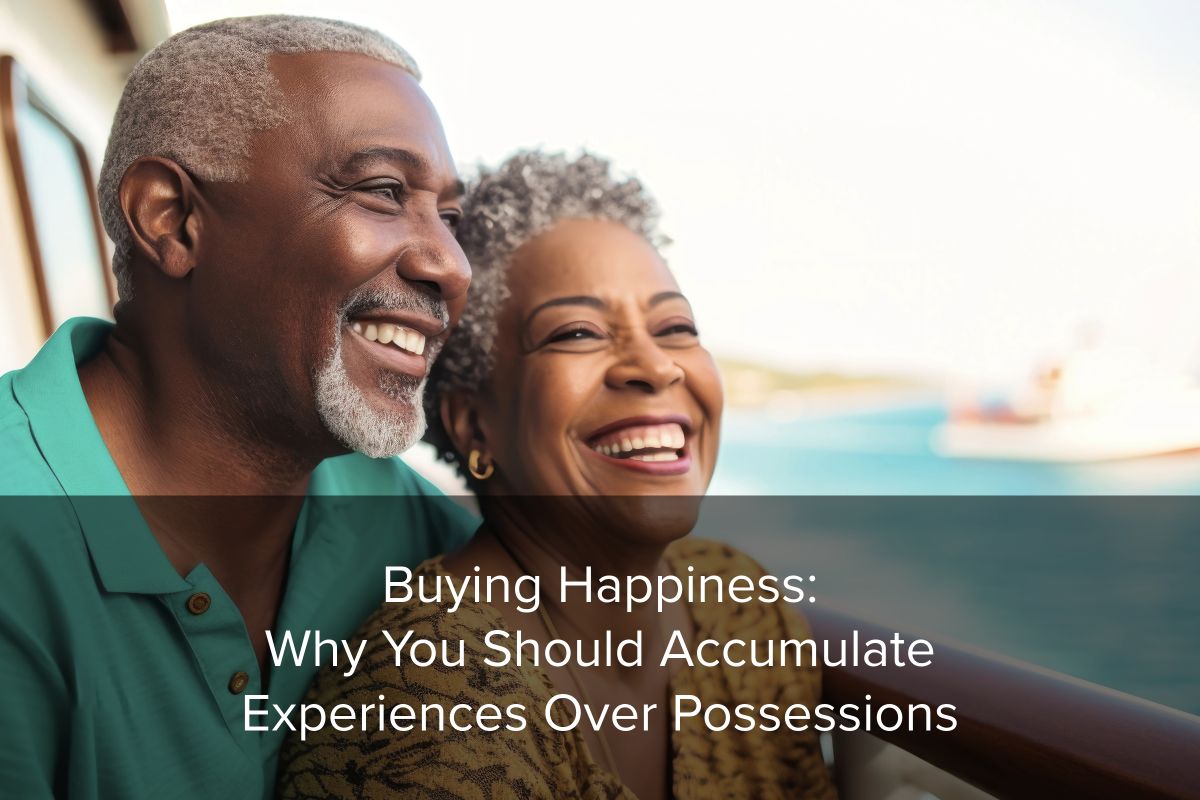

It’s an innate human condition to search for self-fulfillment and experience true happiness in our lives. As long as civilization has existed, the question of how to achieve this has remained somewhat elusive. Can money buy happiness? Well, in some ways it may. In this article, we’ll look at how

Retirement is a major phase of transition, and it’s likely that the day-to-day routine that you’ve been so accustomed to over the years will change dramatically. Although you may have planned for the financial aspects of retirement, it’s just as important to adopt a retirement mindset that will help you

Financial stress and anxiety are things we all experience at times. When our lives go through major upheaval or big changes, such as divorce or the arrival of a new baby, these feelings can be difficult to manage. Not only can these feelings impact our finances in negative ways, but