While the recent volatility in the stock market, the likelihood of an economic recession, and the proliferation of a global pandemic has had a deep impact on nearly everyone’s portfolio, our clients experienced little to no impact on their retirement income due to our three-bucket investment approach.

Here’s how: our number one focus at TriCapital is to put plans in place to help make sure our clients never run out of money. One of the tools we use to accomplish that goal is our three-bucket approach to asset allocation. Since 1926, large stocks have returned about 10% per year while government bonds have returned between 5% and 6%i so we want our clients to have a significant allocation to stocks in order to benefit from the higher return. However, stocks are also more volatile than bonds and we don’t want to have to sell stocks in order to produce the income our clients need when they are down a lot. To deal with this challenge, we divide our clients’ portfolios into three “buckets”. Here’s a description of each bucket and the process we use to manage our clients’ retirement income.

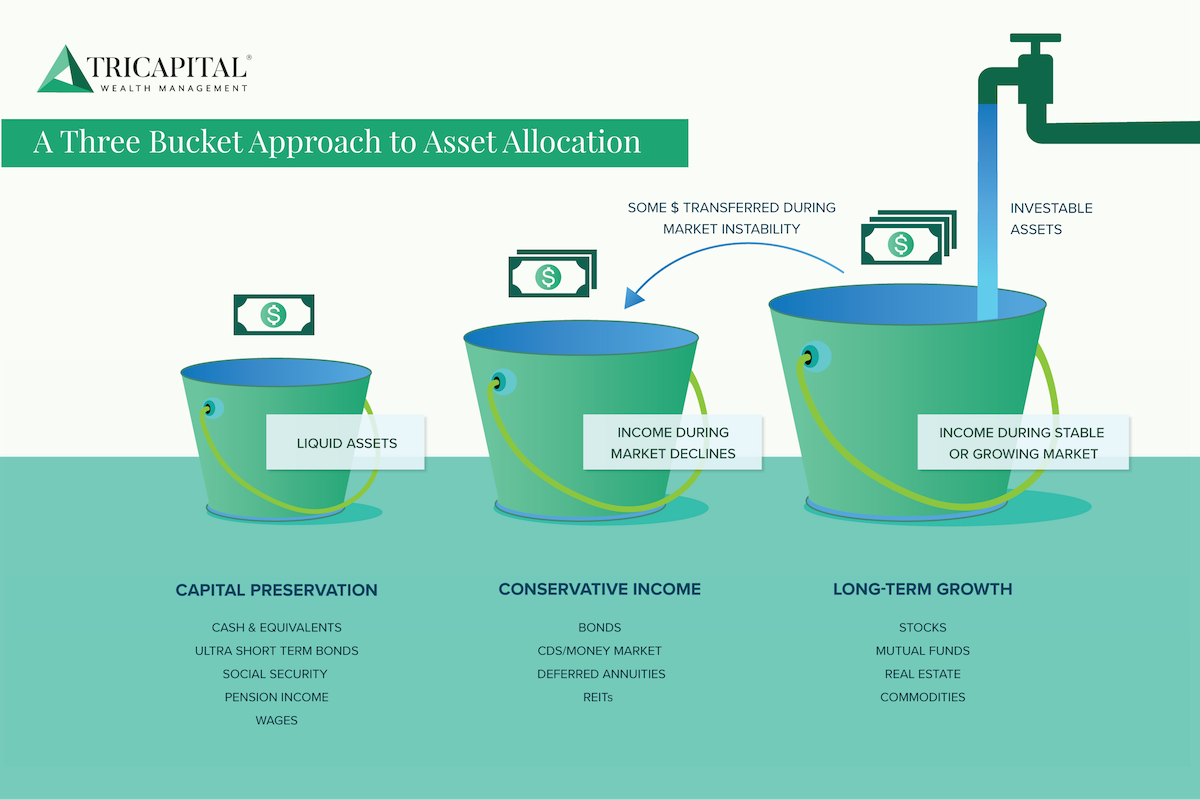

Bucket 1: Contingency

Bucket 1 is money set aside for contingency purposes. This is funded with cash, money market, and ultra-short-term investments in order to be readily available with little or no penalty. This bucket can be helpful if you need immediate cash for unexpected expenses or emergencies that cannot be funded by your established retirement income stream coming from Buckets 3 and 2.

Bucket 2: Income Protection

Bucket 2 is invested in various types of bonds and other fixed-income investments and is what we refer to as a “side fund”. This is because the majority of your retirement income will be taken from Bucket 3, but during periods when the stock market is down significantly as it was recently, we shift to taking your income from Bucket 2 instead of Bucket 3. When the market drops quickly and sharply as it did in recent weeks, we draw your income from this bucket because is it the most stable. When the investments in bucket 3 (mostly equities) drop in value, drawing income from Bucket 2 allows Bucket 3 the time it needs to recover its value while you continue to receive a stable income. The amount allocated to Bucket 2 is unique to your risk profile which we establish for every client we serve by having them complete a Riskalyze Questionnaire. You can take yours here to get started on your Three-Bucket approach to Retirement Planning.

Bucket 3: Income Growth

The majority of your investable assets are allocated to Bucket 3 which consists of stocks and stock mutual funds. Why? Because the equities that make up the investment strategy of Bucket 3 are what drive the long-term growth of your wealth. During periods of growth and relative stability in the markets, this is also where we draw your retirement income. As described above, during times like the recent market plunge we switch from Bucket 3 to Bucket 2 for income distributions so that Bucket 3 has the time to recover its value. Typically, this switch takes place when the market is down in excess of 15%. Once we begin to see a stable recovery, we replenish Bucket 2 from Bucket 3 and resume business as usual.

There is a critical reasoning behind this approach. The old adage buy low, sell high is not a cliché, but rather gospel. The last thing that you want to do when the market drops is have to sell your stocks when they are down in order to produce the income you need. Our strategy allows you to ride out even substantial market downturns without having to lose out on the opportunity for growth that eventually arises from corrections.

Process

Our process to implement the Three-Bucket approach works like this: We first do some analysis to understand the assets you have and the income you need to live the lifestyle you want. Step 2 involves understanding your risk tolerance and we have a well-defined process to do that. Once this is accomplished, we help you fund Bucket 1, and then we allocate your investment assets to Buckets 2 and 3. When you are ready to begin receiving income from your portfolio, we set up distributions to you from Bucket 3 and continue those as long as the market is up, flat, or down within established parameters. In periods where the stock market is down substantially, we shift to taking income distributions from Bucket 2 until the stock market recovers. Once the stock market recovers substantially, we replenish Bucket 2 and resume taking income distributions from Bucket 3. This process is intended to allow us to position as much of your assets in stocks as fits your circumstances so that you get as much growth as possible while providing a framework to avoid having to sell stocks for income when they are down substantially.

Summary

We at TriCapital believe stocks provide superior returns over bonds over the long term and we want our clients to benefit from that performance. We also recognize that bonds are useful in funding known capital needs in addition to providing a stable base from which income can be produced during stock market turmoil. Our goal is to grow your income base, produce the income you need, and allow you to sleep well at night knowing your income will continue no matter what economic shakeups take place. There’s always another market shakeup on the horizon and we want to be ready for whatever that brings.

As always, we are here to answer your questions and be there for you through good times, bad times, and these unprecedented times. We offer complimentary retirement plan reviews and discovery call consultations to those who can appropriately benefit from our services. To find out if our approach can be helpful to you, complete our Riskalyze Questionnaire and a member of our team will contact you with the next steps.

i https://money.cnn.com/retirement/guide/investing_bonds.moneymag/index3.htm

Securities offered through Triad Advisors, LLC, member FINRA/SPIC. Advisory services offered through TriCapital Wealth Management, Inc. TriCapital Wealth Management, Inc. is not affiliated with Triad Advisors, LLC.