Retirement is a time when people can take some time for themselves and travel, spend more time on hobbies and leisure activities, start a side business, volunteer or go back to school. Whatever your goals are in retirement it is also important to keep ongoing retirement planning in mind even after you have blown out those candles.

There can often be the mindset that you’ve done all of your planning and now it’s on autopilot so you can sit back and enjoy the ride. While this is partially true, especially if you have been proactive about your retirement planning for many years, it is important to keep your goals and your plans to achieve them firmly in sight.

Your Retirement Spending Plan

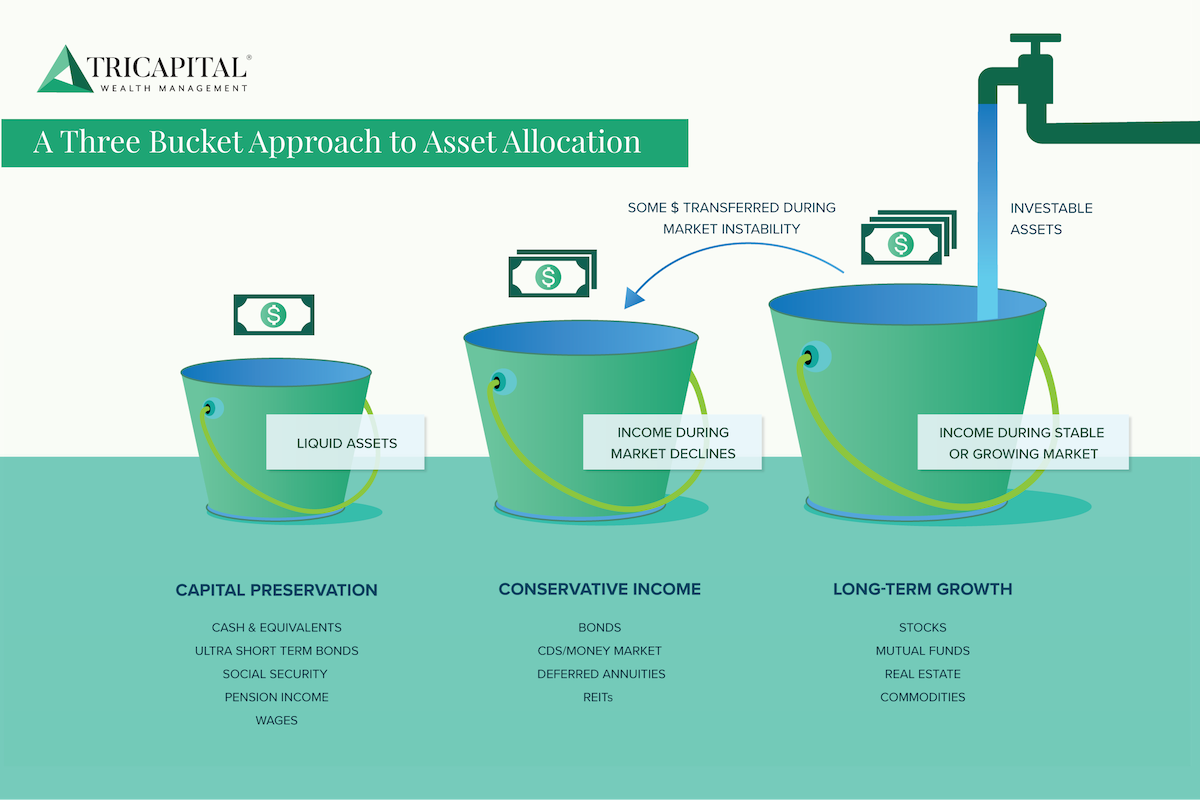

As you move from saving to spending your retirement assets, consider how you will divide your assets over time. Often referred to as the bucket approach, categorizing your time and your assets into “buckets” can help you plan ahead for the long term. Our approach to the retirement spending plan is different than the traditional 3 bucket approach as outlined in the graphic above.

Bucket 1 is used for your capital preservation

The money that goes in Bucket 1 should be liquid or in ultra-short-term investments in order to be available easily with little or no penalty. It would be used in the event of large unexpected expenses. If and when it is used this fund will be replenished by Bucket 2 in an unstable market environment or by Bucket 3 in stable and growing market periods.

Buckets 2 and 3 are where your retirement income comes from.

Bucket 2 is comprised mostly of fixed income investments and is used as the source of your retirement income during steep market declines when the investments in Bucket 3 drop in value. The amount retained in Bucket 2 is unique to your risk profile. Using funds from Bucket 2 instead of Bucket 3 during periods when stocks are down allow the assets in Bucket 3 to recover in value while you continue to receive a stable income. This way the bulk of your assets can stay invested in stocks and have the time to recover from the market decline.

Bucket 3 is where we place the majority of your investable assets. This bucket is invested mostly in stocks in order to achieve the long-term growth that you need for your income to continue to grow. We produce your income from this bucket as long as the stock market is up, flat, or down 10% or less. In times when the stock market is down more than approximately 10%, we shift to produce your income from Bucket 2 until the stock market recovers. Then we replenish Bucket 2 and resume producing your income from Bucket 3. This way you are always positioned to ride out significant market declines without having to sell stocks when they are down.

Set Your Priorities

It should go without saying that establishing which items are needs and which are wants is critical to creating and maintaining a healthy retirement plan. While we all want to live our “dream retirement”, being realistic about how much you can spend after you are meeting your current needs and saving for needs that may arise in the future is important to outliving your retirement savings.

Having a keen understanding of this can also help you to realize that you may have more than what you thought you needed at the outset. Some people think they need more than they actually do and are overly cautious about funding their rainy-day fund. Maintaining a saving mindset in retirement is healthy but suffocating yourself with fear of losing or not having enough is not healthy. Your retirement is an opportunity to loosen up, try new things and relax. Having a solid understanding of what your finances can afford is the best way of finding happiness and confidence.

Have a Plan and Understand What it Means

Having an outlined set of goals and an action plan for achieving them can help you keep your retirement savings working for you and giving you confidence for what lies ahead. The best thing that you can do in retirement is to keep yourself well informed of the state of your plan by reviewing it annually with your financial advisor and being flexible to make adjustments when life changes course.

We can help to guide you through the process and establish a clear path forward as you embark on your new retirement. If you are interested in setting up a complimentary review of your existing financial plan and portfolio please contact us.

Securities offered through Triad Advisors, LLC, member FINRA/SPIC. Advisory services offered through TriCapital Wealth Management, Inc. TriCapital Wealth Management, Inc. is not affiliated with Triad Advisors, LLC.